$COUR: An Education in Value Investing?

$COUR: An Education in Value Investing?

Why Coursera could be a hidden gem in a beaten down sector

EdTech has been absolutely crushed in the public markets following the launch of ChatGPT and given the disruptive nature AI. However, I believe not all EdTech is created equal and Coursera (ticker: COUR 0.00%↑) stands apart from the crowd as an incredibly unique value proposition amid the sector-wide recession.

We are going to outline our thesis and evaluate the stock from 5 key focus areas: (1) Revenue Growth (2) Earnings Growth (3) Balance Sheet Strength (4) Free Cash Flow (5) Valuation.

TL;DR

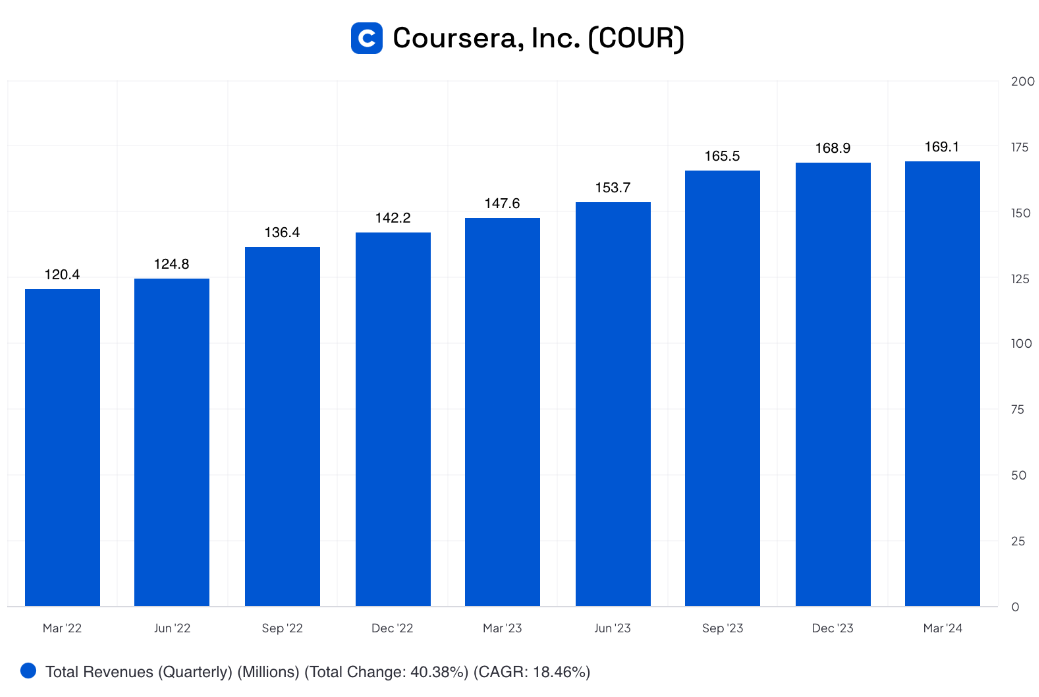

Over the past 2 years, quarterly top-line revenue growth remains strong at an 18.5% CAGR

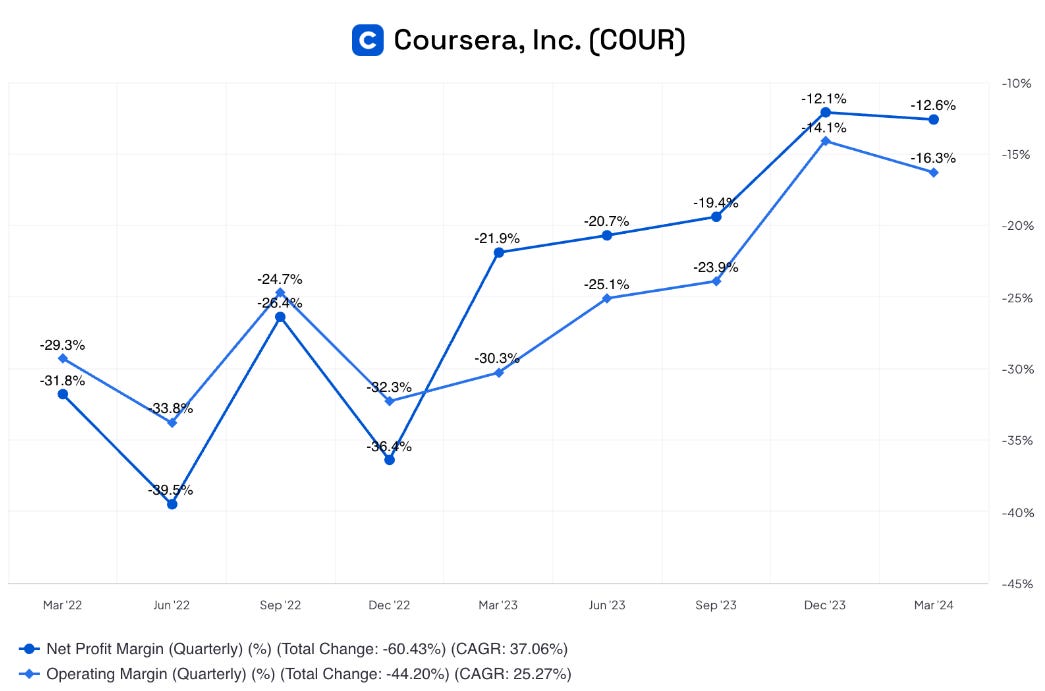

Coursera continues to trend towards consistent profitability, growing its quarterly net profit margin by a 37.1% CAGR in the last 2 years

Courera has $725M in cash on the balance sheet, meaning the company trades at < 1.5x cash

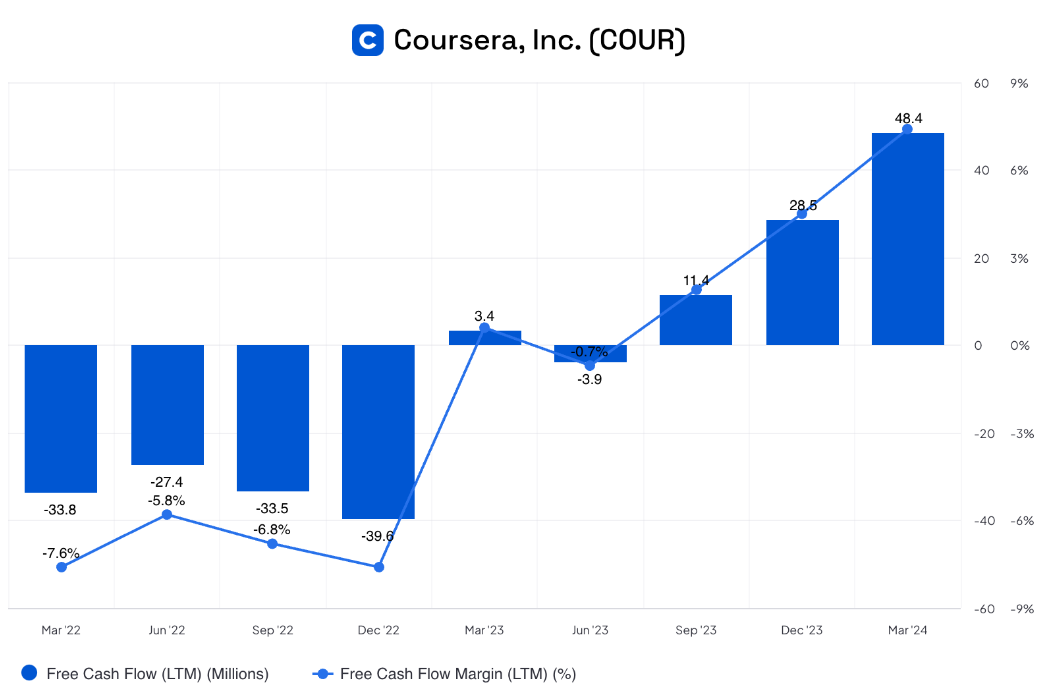

Coursera is FCF margin positive as of FY2023 at 4.5% and most recently at 7.4% in the trailing twelve months (“TTM”)

EV/forward revenue multiple of 0.5x compared to 2.6x for the average of public EdTech companies (EV/forward FCF of 15.4x vs. 27.4x average)

As always, subscribe if you enjoy the content and join the discussion!

The High Level Thesis

Coursera is down 85% since its IPO in 2022 and down 65% in 2024 alone. Analyst downgrades have intensified the fear of disruption from AI, most recently with Goldman Sachs’ downgrade in January of this year.

I believe the company is largely being ‘penalized’ by the market in two core areas: potential impact of Generative AI and lack of long-term, consistent profitability. I believe these concerns are largely overblown and AI could instead be a major catalyst for Coursera.

The Narrative is Backwards

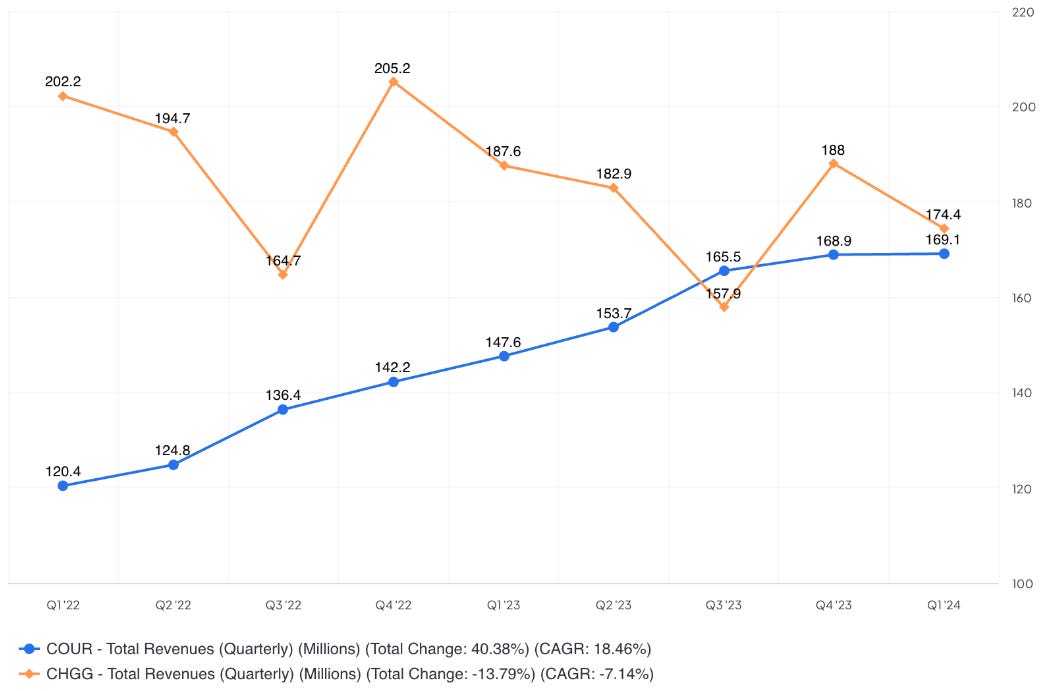

Generative AI should be an enabler for Coursera and not a disruptor as the market is pricing in. Businesses like Chegg (ticker CHGG 0.00%↑) are more directly impacted by the likes of ChatGPT in my view because they directly compete on the “chat-like” interface of homework/study assistance. For example, now you just show ChatGPT your homework question or essay topic and it can immediately provide assistance.

Coursera on the other hand provides personalized learning services. Consumers aren’t simply looking for answers or assistance with a tangible output. Instead, Coursera’s users are seeking self improvement.

In the Enterprise and Degree business segments, AI already acts as a catalyst for growth, allowing Coursera to embed unique services/tooling to their customers with AI.

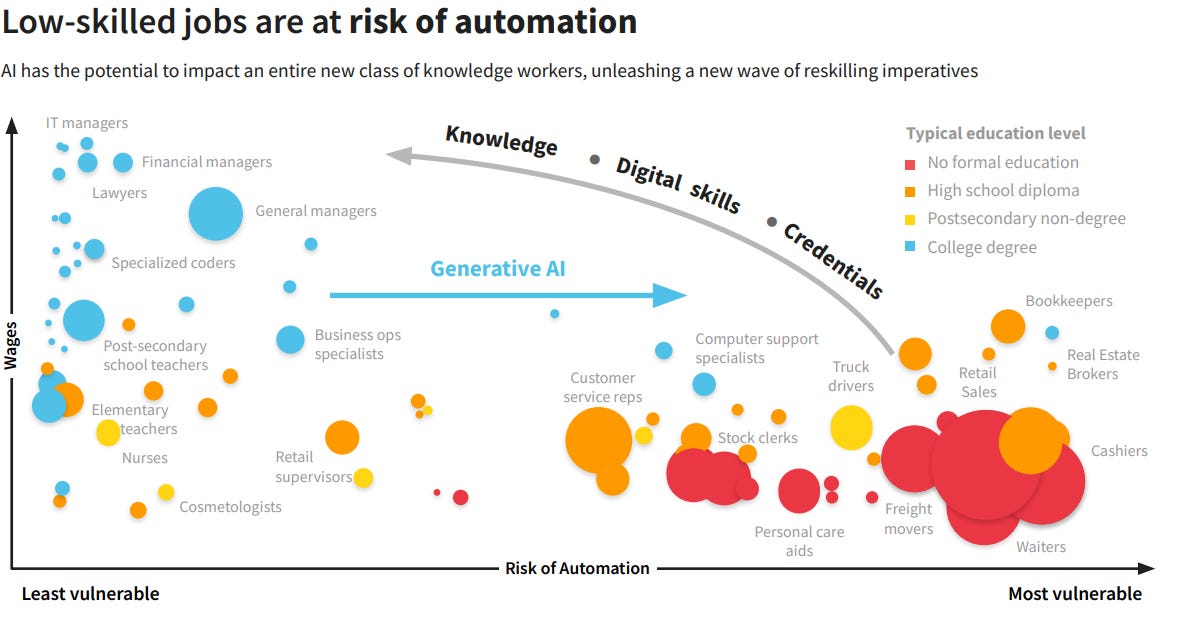

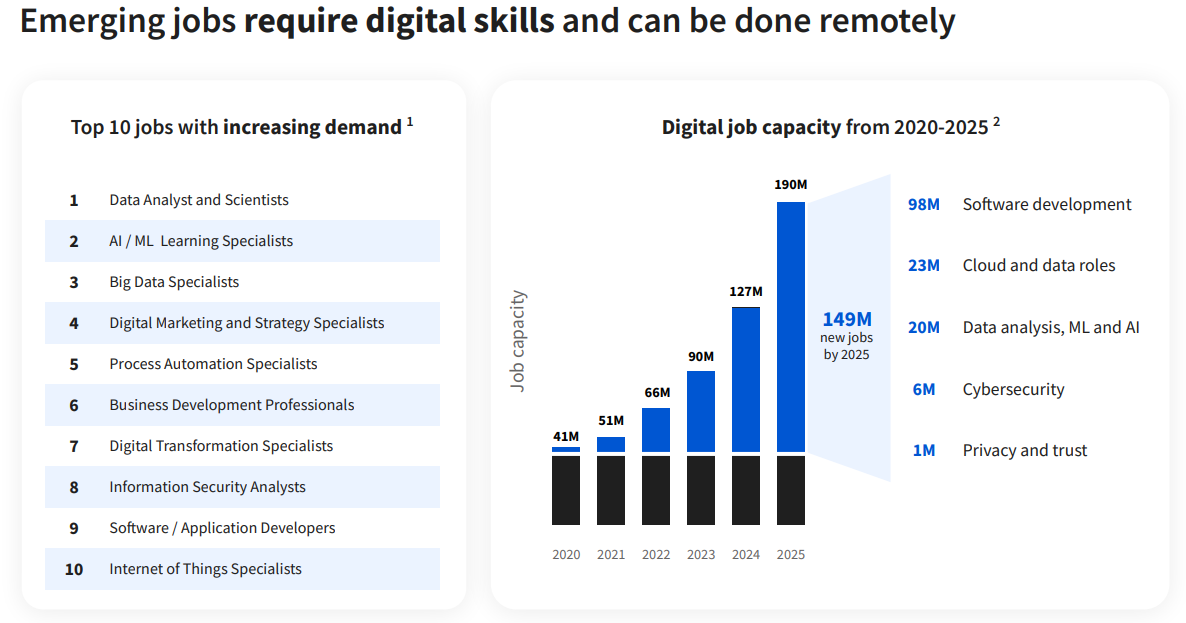

Workforce Re-skilling

Assuming AI continues to disrupt “white collar” jobs, ongoing education and re-skilling will become increasingly important. Coursera offers degrees and certifications that provide its users with credentials that then make them more competitive in the job market. This should act as a major catalyst to Coursera’s convenient online learning platform.

Partners like IBM, Google, AWS, Microsoft and Meta already leverage Coursera to launch these professional certifications.

Leadership is Deeply Rooted in ML/AI

A key piece I believe many miss with Coursera is in their very founding. Andrew Ng, the founder and now Chairman of the company, is one of the most respected minds in machine learning and AI. He has been one of the largest proponents of AI education and quite literally runs one of the top venture funds focused on ML & AI via the AI Fund. I believe he remains a major competitive resource and advantage for Coursera.

Revenue Growth

Despite the narrative that Generative AI will be a major disruptor to Coursera, the company continues to compound quarterly revenue by 18.5% over the past 2 years, showing no signs that AI is killing its business.

To exaggerate the point, compare this with Chegg who I believe is directly impacted by ChatGPT (for the reasons previously outlined). Chegg’s revenues have declined by a quarterly average of 7.1% over the last 2 years.

As I believe AI will be a tailwind to Coursera and not a disruptor, I see no reason to believe that revenue will not continue to grow at a steady clip in the coming years. Management continues to provide positive guidance at 10%+ growth going forward.

While this is below the levels of the last several years, the actual contributor is likely the broader slowdown in general software spending amid the difficult macro (more B2B impacted than consumer in all likelihood, but you get the point). If you’ve followed software earnings this last quarter, it wasn’t pretty.

The general point here is that the business is still very much growing and AI is not hurting the business, contrary to the media narratives.

→ PASS

Earnings Growth

While I don’t believe the narrative that AI is a disruptor to Coursera, I do think that the market is valid in wanting to see more consistent profitability and growth in earnings.

However, over the last 2 years, Coursera has consistently improved its net profit margin, growing at a quarterly rate of 37.1% over that period. While the net profit margin is still negative at -12.6%, the business has come a long way since going public and the margin is improving at near 2x the rate of top-line growth, meaning the business is exhibiting strong operating leverage (good sign).

Assuming the trend reasonably continues, Coursera should be able to achieve consistent earnings growth in the years to come.

→ PASS

Balance Sheet Strength

Coursera has $725M in cash on the balance sheet and effectively no debt. As the company currently has a market cap of $1.1B, this means Coursera is trading at ~1.5x cash… Andddd this is where things get really interesting.

As cash flow from operations has been consistently positive over the last 3 quarters, this means Coursera should only get cheaper as a multiple of cash.

→ PASS

Free Cash Flow

Free Cash Flow (“FCF”) represents the cash that a company generates after accounting for capital expenditures to maintain or expand its asset base. It is an important metric for investors because it shows how much cash the company can distribute to its shareholders without harming its growth prospects.

The cash reflected in FCF can be used in several ways to reward shareholders:

Dividends: This is a direct form of reward where cash is distributed to shareholders.

Buybacks: The company can buy back its own shares from the market, which can potentially increase the stock's value and benefit shareholders via reduced share count.

Reinvestment into the Business: The company might reinvest in its operations to drive growth, which can lead to increased future earnings and potentially higher stock prices.

As Courera is still a young business working to achieve scale, dividends are out of the question (likely for many years). However, it is important to note that FCF can be used to accelerate share buybacks, and in Coursera’s case, this could be extremely beneficial to shareholders.

In Q1 2023, Coursera approved a $95M share buyback program. Per the April 2024 earnings transcript, the company has $15M remaining under the total repurchase authorization, which is expected to be complete in Q2.

This demonstrates management is willing to buyback shares at attractive valuations and I wouldn’t be surprised if they announce a similar buyback program this summer. The share price is meaningfully compressed and as FCF generation is increasingly positive, the company should be able to meaningfully repurchase shares through year end. Combining the FCF generation with the strong balance sheet, and I have no doubt management will strongly evaluate a major buyback program to stabilize the share price.

Coursera also has a very high and increasing FCF yield of 7.4% (inversely related to the earnings multiple).

When a company has a high FCF yield, it suggests that a larger proportion of its valuation is backed by cash that can potentially be distributed to shareholders. This means that even if the stock's price appreciation (capital gains) is modest, the total return to investors can still be attractive due to the potential for cash distributions in the form of dividends and buybacks.

Note: Stock-based compensation (“SBC”) has remained extremely high, leading to an increasingly high share count which has a significantly dilutive impact to shareholders. Buybacks have partially offset this in the past, but the company’s share count has increased by 5.6% on average since 2021. SBC in FY2023 was $110M, which is extremely high for a business with a $1.1B market cap. This is largely a function of the declining stock price, but nonetheless, it’s still very high as a percent of the market cap. I don’t love this personally.

→ PASS

Valuation

Again, Coursera currently trades close to 1.5x cash. This puts COUR 0.00%↑ in MAJOR value territory, and as we’ve explored above, the business is still exhibiting strong growth and simultaneously demonstrating strong profitability. I believe the stock is well oversold on fears of AI disruption, which I believe is misguided.

Coursera also has one of the strongest balance sheets amongst its public EdTech peers, only coming in below Duolingo (ticker: DUOL 0.00%↑) which has $830M of cash on the balance sheet.

Only Duolingo maintains a higher top-line CAGR than Coursera, yet trades at an 18x higher EV/forward revenue multiple. Compared with its close competitor Udemy (ticker: UDMY 0.00%↑), Coursera is growing top-line faster and expanding its net income at almost 3x the rate (while trading much cheaper).

I believe dramatic multiple expansion on EV/forward revenue is reasonable given the expected growth rates and trend towards profitability for the business, especially considering the average EV/forward revenue of its peers sits at a 385% premium at 2.6x vs. 0.5x for Coursera (mind you, the 2.6x includes Coursera, so it’s very conservative).

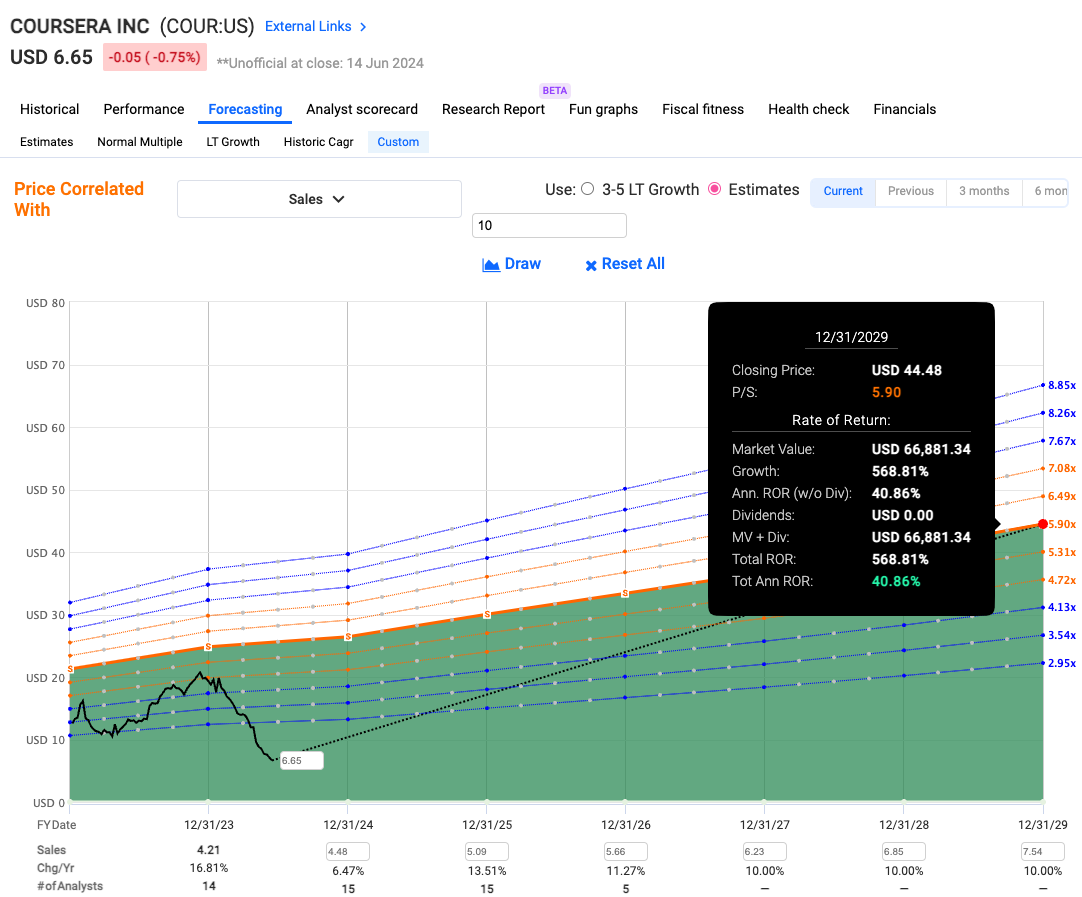

Note: In the return chart above, the multiple is plotted as Price/Sales, which differs from EV/Revenue. The multiple expansion was applied to the blended P/S ratio of 1.5x to get the benchmark 5.9x. Blended P/S is based on the average of LTM and NTM revenue.

Assumptions are as follows:

5-Year Sales CAGR: 10.5%

P/S Multiple: 5.9x

The return model is essentially going to assume a meaningfully lower revenue growth rate over time (reminder: 2-year quarterly CAGR was closer to 18.5%).

Assuming a 5.9x P/S as a benchmark, which is based on the reversion to the average of Coursera’s peer group multiple (see note above below chart).

In the return model, where the business performs well (but below the rates of the last several years), I would anticipate Coursera to compound close to 40.9% annually though CY2029, leading to a near 7x in just over 5 years.

Concluding Thoughts

The general takeaway is that Courera trades at such compressed valuations for what I believe to be the false pretense that AI will majorly disrupt their business model. When you look at the discrepancy of growth and performance relative to Chegg since the launch of ChatGPT, it becomes very apparent that this is a business that continues to exhibit strong top-line growth and is reaching scale such that the business should produce more predictable FCF going forward. In other words, I believe the market is wrong in AI’s impact to Coursera.

Furthermore, the company trades SO low at just 1.5x its cash, that the upsize is IMMENSE. Multiple expansion alone is a major benefit to investing in Coursera at this valuation and why I believe the stock is a major value play in the EdTech industry.

Join the discussion and let me know your thoughts!

Thx! Keep up the good work.